As the first quarter of 2024 concluded, the financial markets demonstrated resilience amidst cautious optimism and economic complexities. March showcased divergent inflation trends, with the U.S. experiencing higher-than-expected inflation in contrast to Canada, where inflation cooled and aligned more closely with the Bank of Canada’s (BoC) expectations. Despite central bankers starting discussions around potential rate cuts, a cautious stance is likely to prevail, particularly given the backdrop of elevated wage gains. The inflation outlook indicates an uneven path ahead, with the U.S. inflation forecast for 2024 being revised upwards to an average of 3.1%, while Canada’s forecast has been adjusted downwards to 2.6%.

On the other hand, the stock market continued its upward trajectory, rallying despite challenges such as rising interest rates and inflation concerns. Bolstered by a strong U.S. economy and the prospects of a soft landing, investor enthusiasm has been particularly noticeable in mega-cap companies and the booming artificial intelligence industry. Although market momentum may seem overbought, positive seasonal trends and historical patterns indicate potential for continued growth, suggesting that this rally could sustain its viability in the medium or long term.

Monetary policy remains a critical area of focus, especially with the Bank of Canada expected to potentially cut rates ahead of the Federal Reserve, reflecting Canada’s stronger economic position and more favorable inflation dynamics. Market expectations are heavily tilted towards a June rate cut, with the BoC anticipated to reduce rates by 100 basis points to 4.00% by the year’s end, signaling more aggressive action compared to the Fed, which is expected to make three cuts totaling a 75 basis point decrease.

| Index | Feb-2024 | Mar-2024 |

| S&P 500 Total Return | 5.34% | 3.22% |

| S&P/TSX Total Return | 1.82% | 4.14% |

Canada

In March 2024, the S&P/TSX Total Return Index experienced a notable 4.14% increase, reinforcing the Canadian economy’s strong beginning to the year. This upward trajectory builds on January’s robust GDP growth of 0.6%, which exceeded expectations and represented the highest rate of expansion in twelve months. Furthermore, preliminary figures for February indicate the momentum continued, with the economy again expanding by an impressive 0.4%. This back-to-back growth, amounting to a 1.0% increase over just two months, matches the total growth achieved throughout the entirety of 2023. The Bank of Canada maintained its prime overnight rate at 5%, aligning with expectations but diminishing borrowers’ hopes for easing, due to persistent core inflation concerns. Governor Tiff Macklem indicated that the Governing Council’s debate has evolved from questioning the sufficiency of the restrictive rates to deliberating on the duration for which they should remain at the present level. Although the inflation rate has decreased from a peak of 8.1% in June 2022 to under 3%, pressures on prices, particularly from housing costs and salaries, are still escalating. According to Macklem, it is necessary to allow more time to secure a decline in inflation towards the bank’s target of 2%.

Inflation Trends: February saw a modest dip in headline CPI inflation to 2.8% on a year-over-year basis, contrary to projections of an increase. A notable decrease in grocery store inflation contributed to this change, with prices rising by 2.4% compared to 3.4% in the previous month, marking the first instance since 2021 where grocery price inflation fell beneath the overall inflation rate. Additionally, core inflation also experienced a decrease, averaging 3.2% year-over-year, a drop from January’s 3.4%.

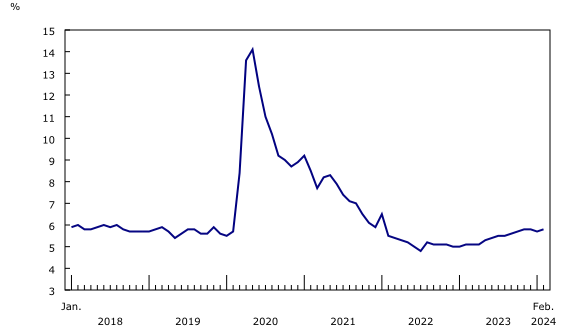

Job Market: In February, the Canadian job market saw the creation of 40,700 new positions, all attributed to full-time employment, which led to a slight increase in the unemployment rate to 5.8%, according to data from Statistics Canada. The goods-producing sector experienced a decline, losing 6,300 jobs, predominantly in manufacturing, while the services sector gained 46,900 jobs. Wage growth in Canada remained significant, with average hourly earnings increasing by 5% over the past year, slightly down from January’s 5.3% growth rate.

Source: Statistics Canada

Manufacturing Sector: A modest increase was observed in the manufacturing sector in January, with sales ticking up by 0.2% to reach $71.1 billion. This growth was primarily driven by the motor vehicle and chemical manufacturing subsectors, as reported by Statistics Canada.

Consumer Spending: January witnessed a slight contraction in Canadian retail sales, less severe than anticipated, affected by reduced prices and sales in the motor vehicle and parts segment. Retail sales saw a decrease of 0.3% following December’s 0.9% rise, buoyed by holiday shopping. Preliminary data for February suggest a modest rebound in sales, with an expected increase of 0.1%.

United States

The S&P 500 Total Return Index market has seen remarkable growth of 3.22% in March. The bull market returned about 50% since its inception in October 2022, driven by an improved economic and earnings outlook. Despite high valuations, strong fundamentals have sustained market momentum. Key contributors to this rally include Artificial Intelligence stocks, bank stocks, and dividend-paying stocks, which collectively propelled equity markets upwards in March.

Investor focus in March also turned to the Fed’s meeting, amid concerns over consecutive inflation reports exceeding estimates. The Federal Reserve maintained its short-term interest rates, aligning with market expectations. However, it introduced an outlook of three quarter-point rate cuts within the year, depending on the services inflation trend and the potential growth risks. This suggests that rates could remain higher for an extended period, with the Federal Open Market Committee (FOMC) indicating a possibility of rates being higher in 2025 than previously projected. Despite this cautious stance, the Fed’s revised economic projections for 2024 are more optimistic, with GDP growth expectations lifted from 1.4% to 2.1%, signaling cooling inflation pressures but a bumpy journey toward the 2% inflation goal. Additionally, economic indicators further complicated the landscape.

Labor market: Data revealed some softening with the unemployment rate in the U.S. climbing by 0.2% to 3.9% in February, marking a two-year peak. The tally of individuals unemployed for a longer duration rose by 174,000, reaching 1.7 million, the highest since November 2021. Meanwhile, nonfarm payroll employment exceeded expectations, adding 275,000 jobs compared to the anticipated 200,000, surpassing the 12-month average monthly gain of 230,000. Moreover, employment figures for January and December were adjusted downward to 229,000 and 290,000, respectively.

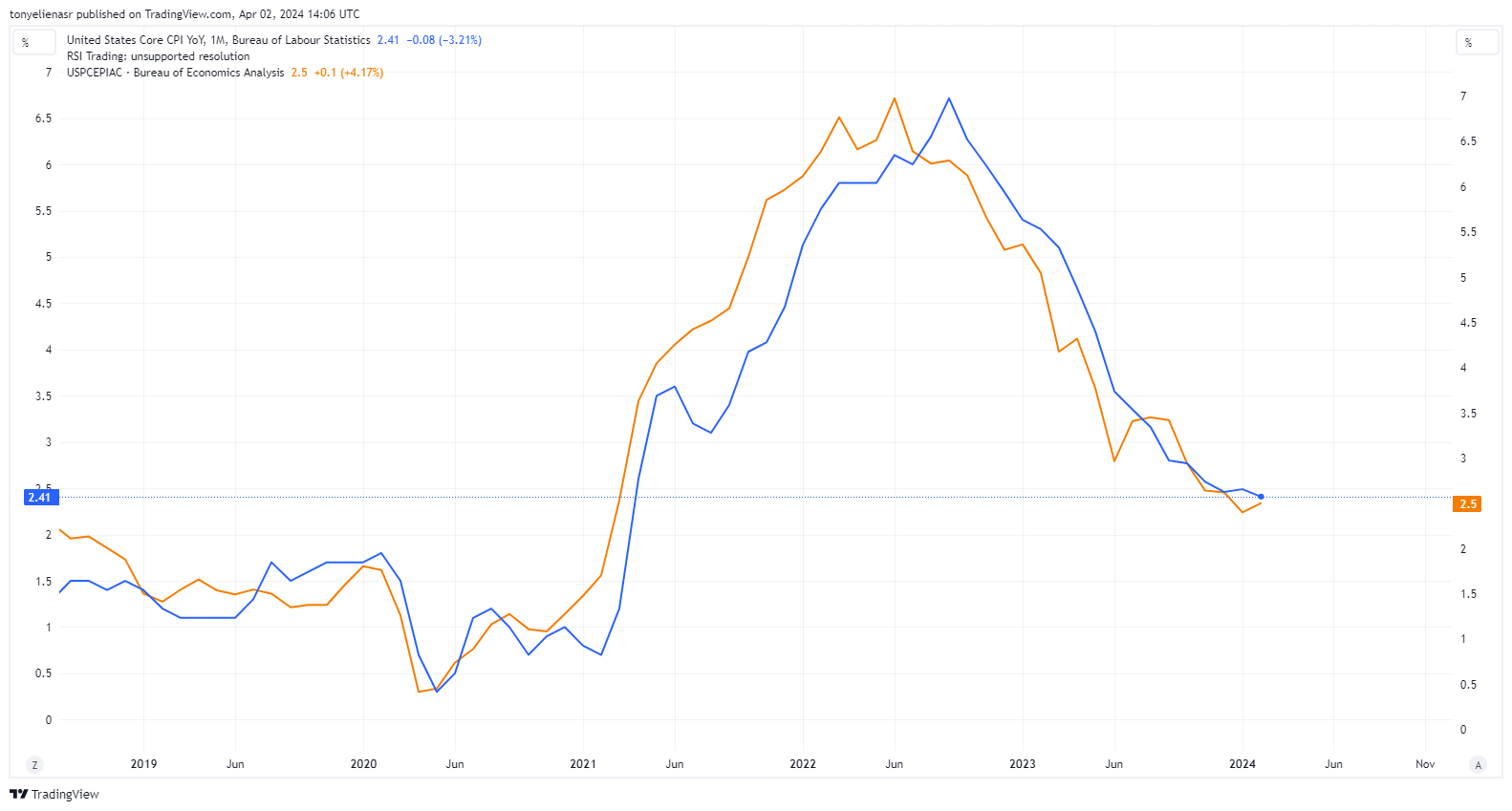

Inflation: February’s Consumer Price Index (CPI) increase exceeded expectations, with a 0.4% month-on-month rise. This resulted in an annual rate of 3.2%, while the increase in core inflation metrics moderated slightly. On the other hand, the Personal Consumption Expenditures (PCE) price index, the Fed’s preferred inflation measure, ticked up to 2.5% year-on-year. February also saw a notable rise in the Producer Price Index (PPI) for final demand. The PPI surged 0.6% from the previous month, with a year-on-year increase of 1.6%, the most considerable annual gain since September.

Retail sales experienced a 0.6% increase in February, rebounding from a revised 1.1% decrease in January, affected partly by adverse weather. The rise was aided by higher gasoline prices, increased auto sales, and a recovery in building materials sales, which January’s severe weather conditions had impacted. Excluding gasoline stations and auto dealers, sales saw a 0.3% increase.

Manufacturing: The Institute for Supply Management (ISM) reported its manufacturing PMI at 50.3 last month compared to 47.8 in February, marking the first reading above 50 since September 2022 and ending 16 consecutive months of contraction in manufacturing. While this rebound in manufacturing is encouraging for economic growth, an increase in raw material prices could signal a rise in goods inflation in the coming months.

Economic Growth: The Bureau of Economic Analysis updated the growth rate of the gross domestic product (GDP) for the last quarter of 2023 to an annualized rate of 3.4%, a slight increase from the preliminary figure of 3.2%. This adjustment comes as consumer spending, a major driver of U.S. economic activity comprising over two-thirds of the economy, was revised to show a 3.3% growth rate. Initially this spending was thought to have expanded at a 3.0% rate, with the revision attributed primarily to the services sector. The quarter saw widespread contributions to economic expansion across various sectors, with nondurable goods manufacturing at the forefront, followed by significant inputs from the retail trade, durable goods manufacturing, and the healthcare and social assistance sectors.

International Markets

In March, international markets witnessed a positive trend despite signs of a slowdown across major global economies. Central banks have begun to explore the possibility of reducing interest rates, proceeding with caution due to ongoing inflation concerns. Geopolitical tensions, especially in the Middle East and the ongoing conflict between Russia and Ukraine, notably, drone strikes on Russian oil facilities, have kept the oil market under strain, resulting in a sustained risk premium. Additionally, a sharp increase in cocoa prices has been observed, attributed to severe supply constraints, which stands out as a significant development in the agricultural commodities market. Gold prices have reached record highs, driven by anticipations of lower interest rates, geopolitical uncertainties, and strategic diversification moves by central banks.

Europe: The euro faced downward pressure, hitting new lows for the month as differences in monetary policy between the US and the eurozone became more pronounced. The swaps market anticipates nearly four rate cuts by the European Central Bank this year, outpacing the expectations for the Federal Reserve. Despite Eurozone unemployment holding steady at a low of 6.4%, economic growth has stagnated since the end of the third quarter in 2022, signaling potential concerns over productivity. Inflation, although moderating from a 6% annualized pace in the first quarter of 2023 to around 4.4% in the first quarter of 2024, remains a focal point for policy adjustments. Political dynamics across EU nations are also shifting, with increasing support for far-right parties and adjustments in fiscal policies reflecting broader economic and social strategies.

Japan: The Bank of Japan (BOJ) undertook a historic rate hike, its first in 17 years, though it barely impacted the yen’s continued depreciation to a new 34-year low. Despite ending its Yield Curve Control and ETF purchases, the BOJ’s commitment to maintaining a highly accommodative policy stance and Japan’s position as a low-yielder kept the yen weak. As such, this weakness prompted verbal interventions from the BOJ and the Ministry of Finance, hinting at the persistent risk of direct market intervention. Meanwhile, February’s retail sales surge indicates a rebound in consumer spending, offering a glimpse of economic resilience amidst challenges.

United Kingdom: The UK economy shows signs of recovery in the first quarter after previous contractions, with price pressures expected to significantly ease into the third quarter. February saw the annual inflation rate drop significantly to 3.4%, a sharp decrease from the previous year’s 10.4%. This reduction was largely influenced by decreased costs in energy, food, and non-energy industrial products. Indicators such as the S&P Global Purchasing Managers Index suggest a resurgence in economic activity in the first quarter, moving past the technical recession witnessed at the close of 2023. This recovery is particularly noted within the services sectors, hinting at a positive turnaround.

China: While global stock markets have seen robust returns, China’s market is underperforming amid ongoing real estate concerns. Recent data, however, signals recovery, with a noteworthy 10.2% profit increase for industrial firms in early 2023, rebounding from the previous year’s decline, supported by government actions and stronger foreign demand. Other positive economic indicators include growth in industrial output, investments, and consumer spending. Yet, deflationary risks and the real estate downturn continue to dampen investor sentiment. The excessive market pessimism challenges policymakers to boost confidence and address the economic issues.

The Portfolio Management Team