The economic disparity between the U.S. and Canada persisted throughout May. Inflation in the U.S. remains persistently elevated, but recent indicators suggest a potential cooling trend. However, the Federal Reserve will require more significant progress before contemplating an easing of policies. In contrast, Canada’s core inflation trends are showing signs of moderation and a faster pace in reaching the targeted rate. Consequently, the Bank of Canada is anticipated to decrease interest rates on June 5.

Canada’s economy grew less than anticipated in the first quarter, as weak inventory growth countered strong consumption gains. This economic underperformance has led traders to increase their bets on an imminent rate cut by the Bank of Canada. Meanwhile, the U.S. stock market experienced significant volatility in May 2024, with the S&P 500 and Nasdaq Composite reaching record highs multiple times. This was largely driven by robust performances from major technology companies, often referred to as the “Magnificent 7” — Apple, Amazon, Microsoft, Alphabet, Meta, Tesla, and Nvidia.

These contrasting trends highlight the economic divergence between the two countries. While the U.S. grapples with persistent inflation and market volatility, Canada faces a moderating inflation environment and slower-than-expected economic growth. As a result, the respective central banks are expected to take different monetary policy approaches in the coming months.

| Index | Apr-2024 | May-2024 |

| S&P 500 Total Return | -4.08% | 4.96% |

| S&P/TSX Total Return | -1.82% | 2.55% |

Canada

The Canadian stock market exhibited modest fluctuations in May 2024, reflecting a cautious economic climate. The S&P/TSX Composite Index closed the month higher, registering a 2.55% increase. This positive performance was influenced by a combination of factors, including a moderation in inflation, a growing probability of a rate cut in June, and a robust job market.

Economic growth: Canada’s economy showed a notable slowdown after a strong start to the year. The real GDP growth for the first quarter was 1.7% annualized, falling short of the expected 2%, and the previous quarter’s growth was revised down to 0.1% from the earlier 1.0%. The monthly data reveals a drop from a robust 0.5% increase in January to a moderate 0.2% in February, followed by no growth in March. However, an estimate from StatCan indicates a 0.3% GDP rise in April.

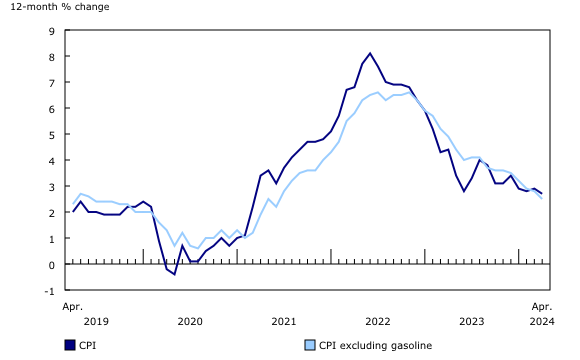

Inflation: Inflation continued to show signs of slowing down, with the headline consumer inflation rate dropping to 2.7% in April. All major core measures also fell below 3%. Grocery prices, which have been a significant contributor to inflation, also continued to moderate, increasing only 1.4% from the previous year, marking the slowest pace since 2021. Tightening monetary policy in Canada has had a consistent impact on underlying inflation. The Bank of Canada now faces the pivotal question of whether inflation has been sufficiently tamed to begin reducing the level of restrictiveness.

Employment: Canada gained an impressive 90,400 new jobs in April, yet the unemployment rate stayed unchanged at 6.1% despite this remarkable job gain. Notably, average hourly wage growth showed a moderation, slowing to 4.7% year-over-year from 5.1%, marking the second-lowest reading in the past year. Geographically, nine out of ten provinces saw job growth, with all four major provinces recording double-digit increases. However, half of the provinces experienced increases in unemployment rates, with Ontario facing a substantial 1.7% increase in the past year, reaching 6.8%.

Retail Sales: Statistics Canada reported that Canadian retail sales experienced a 0.2% decline in March compared to February, reaching C$66.44 billion. This decrease was primarily attributed to reduced sales of furniture, home furnishings, electronics, and appliances. A flash estimate from the agency indicated a probable 0.7% increase in sales for April. Furthermore, retail sales decreased by 0.4% in terms of volume.

Housing Market: In April, Canada experienced a 1% month-over-month decrease in housing starts, resulting in an annualized rate of 240.2k units. Compared to March’s level, this decline is evident. Furthermore, the six-month moving average of housing starts exhibited a 2.2% month-over-month decrease from March, reaching 238.6k units in April. Several factors are contributing to the slowdown, including reduced pre-sale activity in key markets such as Toronto, elevated construction costs, and rising interest rates.

Source: Statistics Canada. Consumer Price Index, monthly, not seasonally adjusted.

United States

In May 2024, the U.S. stock market witnessed remarkable volatility, characterized by substantial gains and notable losses for various stocks. The S&P 500 Total Return Index registered an impressive 4.96% increase, reversing the previous month’s setback. In contrast, the Nasdaq Composite scaled record-breaking heights primarily due to the robust performance of the technology sector. Several prominent companies revealed their quarterly results, and leading tech companies such as Apple and Microsoft have surpassed earnings expectations, contributing to the overall market gains. Moreover, Nvidia reported exceptional financial performance for the first quarter, demonstrating substantial growth compared to previous quarters, attributed to its strategic focus on artificial intelligence (AI) and accelerated computing.

Monetary Policy: The Federal Reserve’s policy decisions remained a focal point for investors. In May, speculation about potential interest rate cuts significantly impacted market sentiment. Some analysts anticipated multiple cuts throughout the year, while others cautioned against overestimating their likelihood. In fact, the Federal Reserve kept rates unchanged in its last FOMC meeting, and market participants initially projected a similar stance for June’s meeting. However, the recent shift in expectations reflects the increased probability of a possible economic slowdown, with investors now predicting a rate cut in September with over 90% certainty. Despite this shift, the Fed remains cautious, emphasizing the delicate balance between economic growth and inflation control as it navigates the monetary policy landscape.

GDP Growth: The US economy experienced a downgraded GDP growth rate in the first quarter of the year. Gross domestic product (GDP) increased by 1.3% annually during the first three months, falling short of the previous estimate of 1.6%, according to the Bureau of Economic Analysis. This deceleration can be largely attributed to a slowdown in personal spending, which grew by 2.0% instead of the initially estimated 2.5%.

Employment: In April, the number of job openings in the United States unexpectedly declined, causing the ratio of available jobs per job seeker to reach its lowest point in nearly three years. This shift in the labor market’s dynamics could potentially assist the Federal Reserve’s efforts to combat inflation. As of the end of April, job openings had decreased by 296,000, bringing the total to 8.059 million, the lowest level since February 2021. Market focus has shifted towards the forthcoming monthly employment report for May, with an unemployment rate projected to hold steady at 3.9%.

Inflation: Last month, the personal consumption expenditures (PCE) price index increased by 0.3%, marking a 2.7% growth over the past year, which is similar to the growth rate in March. In contrast, the core PCE, which excludes food and energy prices, showed a lower-than-expected 0.2% month-to-month increase, falling short of the 0.3% increase analysts had predicted in March. On the other hand, the change in the Consumer Price Index (CPI) experienced a slight decrease in April, from 3.5% in March to 3.4% on an annual basis. The annual core CPI, which excludes volatile food and energy prices, also declined from 3.8% to 3.6% in the same period, aligning with analysts’ estimates.

Consumer confidence: US consumer confidence saw an uptick in May for the first time in four months. This rise occurred despite the prevailing economic woes, particularly inflation, which has consistently impacted consumer sentiments in recent months.

Source: TradingView. US CPI and US PPI Y/Y Change.

International

The international markets experienced varied performances influenced by economic, geopolitical, and sector-specific developments:

European Union (EU): In its spring outlook, the European Commission forecasted a GDP growth of 1.0% for the EU and 0.8% for the euro area in 2024. For 2025, the GDP is anticipated to rise to 1.6% in the EU and 1.4% in the Eurozone. Additionally, the eurozone witnessed a significant development in inflation, as consumer prices increased by 2.6% year-over-year in May, surpassing the consensus estimate of 2.5%. This marks the first time in five months that inflation has climbed. On the employment front, the unemployment rate dipped to an all-time low of 6.4% in April, down from 6.5% in the previous five months.

United Kingdom: The sentiment towards the stock market has turned upbeat, as evidenced by the FTSE 100 index reaching record highs, surpassing the performance of other major indices. However, the annual inflation rate in April 2024 stood at 2.3%, indicating a need for a cautious approach from the Bank of England (BOE) regarding interest rate adjustments. Markets anticipate the first interest rate cut to occur in August, with a potential 0.25% reduction, followed by another potential cut in November.

Japan: In Japan, investors closely monitored the Bank of Japan’s (BoJ) potential monetary policy normalization as the 10-year Japanese government bond yield climbed to 1.07% amid uncertainty surrounding future interest rate hikes. Despite ending its negative interest rate policy in March, the BoJ maintained an accommodative stance. The yen weakened against the U.S. dollar, approaching 34-year lows, with data hinting at government intervention in the currency market on two occasions between April and May to prop up the yen. Although Tokyo’s core consumer price index increased to 1.9% year-on-year in May, primarily due to higher electricity bills, it remained below the BoJ’s 2% target, alleviating the immediate pressure for rate hikes. On a positive note, April’s retail sales outperformed expectations due to rising wages, while industrial output unexpectedly declined.

China: The official manufacturing PMI slid to 49.5 in May from 50.4 in April, indicating contraction, with declines in new orders and exports. The nonmanufacturing PMI also decreased slightly to 51.1, reflecting slower construction growth. Despite these indicators of economic weakness, industrial profits rose by 4% in April, driven by increased overseas demand and domestic upgrades. Economists remain optimistic that China will achieve its growth target of around 5% for the year, supported by the IMF’s upgraded 2024 forecast to 5% from 4.6%.

Oil Market: The oil market has experienced significant volatility amid an uncertain outlook for global supply and demand. Brent crude prices exhibited substantial fluctuations, initially reaching a six-month high above $91 per barrel in April, only to fall below $80 per barrel by the end of May. This decline was primarily driven by concerns regarding the health of the global economy and oil demand, compounded by the persistent geopolitical tensions in the Middle East.

Source: TradingView. EURUSD GBPUSD JPYUSD May Performance.

The Portfolio Management Team