In February 2025, the US economy continued its transition into a slower growth phase, marked by a cooling labor market, persistent inflation, and softening consumer activity. Financial markets remained under pressure as they adjusted to the reality of prolonged high interest rates and muted growth prospects. Adding to the uncertainty, President Donald Trump’s newly imposed tariffs triggered swift retaliatory measures from affected countries, heightening fears of a renewed global trade war.

In Canada, the S&P/TSX Composite Index posted a slight decline, even as the economy outperformed expectations. GDP expanded at an annualized rate of 2.6% in the fourth quarter, driven largely by a rebound in consumer spending. The Canadian economy appears to be responding well to earlier rate cuts, with signs of early-cycle recovery: consumer activity is gaining traction, the housing market has stabilized nationally, and employment growth accelerated into the new year.

Globally, policymakers warned of mounting risks to the world economy from escalating trade tensions, emphasizing the importance of renewed multilateral cooperation to navigate these challenges.

| Index | Jan-2025 | Feb-2025 |

| S&P 500 Total Return | 2.78% | 2.78% |

| S&P/TSX Total Return | 3.48% | 3.48% |

Canada

In February 2025, Canada’s S&P/TSX Composite Index experienced a modest decline, with the Total Return Index decreasing by approximately 0.40%. This downturn is attributed to heightened global trade uncertainties, which have raised concerns about potential impacts on investment and earnings growth.

GDP Growth: Canada’s economy showed strong momentum in late 2024, with fourth-quarter GDP growing 2.6% annualized, outperforming expectations. Growth was supported by robust consumer spending, boosted by rate cuts, and a notable rebound in housing and business investment.

Retail Sales: Canadian retail sales rose sharply by 2.5% in December, marking the strongest increase since 2022, with gains across all sectors and provinces. Higher gas prices led the growth, while categories like food, clothing, and general merchandise also performed well, possibly supported by a tax holiday. Sales volumes climbed at their fastest rate since 2021, adding upside risk to GDP estimates.

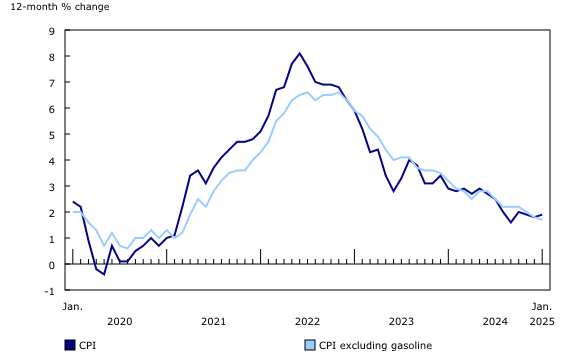

Inflation Trends: Canadian inflation edged up to 1.9% in January, with price increases softened by the GST holiday, though underlying inflation pressures rose to 2.6%. Core inflation also ticked higher, suggesting persistent price growth slightly above the Bank of Canada’s comfort zone. Gasoline, vehicle prices, and phone services saw notable gains, while rents and mortgage costs showed signs of easing.

Source: Statistics Canada. 12-month change in the Consumer Price Index (CPI) and CPI excluding energy

Monetary Policy: After six straight rate cuts totaling 200 bps, including a 25 bps cut in January, the Bank of Canada is expected to pause in March, though rising US tariff risks may push them to continue easing. The central bank has noted that past cuts have already supported household spending, but significant tariffs could strain the economy, prompting further action.

Labor Market: Canada added 76,000 jobs in January, building on strong gains from the previous month and signaling solid momentum in the labor market despite slowing population growth. Full-time employment and total hours worked increased, helping to lower the unemployment rate to 6.6%. Notable job growth in manufacturing and construction, partly driven by tariff concerns, further supported the positive trend. Wage growth eased to 3.5%, the slowest in nearly three years, which may give the Bank of Canada flexibility if trade tensions escalate.

Housing Market: Canada’s housing market was quiet in January, as existing home sales fell 3.3% from December but remained 2.9% higher than a year earlier. New listings increased by 11% month-over-month and 23% compared to last year, pushing the months’ supply of homes to 4.2 from 3.9 in December.

United States

In February 2025, the S&P 500 Total Return Index declined by 1.30% as the economy exhibited signs of cooling. While employment remained robust, there were indications of softening due to persistent inflation and elevated interest rates. Below are the key economic indicators released during the month:

GDP Growth: US economic growth slowed to a 2.3% annualized rate in the fourth quarter, down from 3.1% in the previous quarter, with early 2025 data suggesting further cooling due to the winter weather and growing concerns over tariffs driving up costs.

Inflation: Inflation stayed moderate, with headline PCE up 0.3% and core PCE at 2.6% year-over-year. Meanwhile, the goods trade deficit widened to a record $153 billion due to a 12% import surge ahead of tariffs, raising concerns about growth and tariff-driven inflation.

Source: bea.gov

International

Europe: In February 2025, European equity markets exhibited resilience amid global economic uncertainties, bolstered by robust corporate earnings and a notable surge in defense stocks, which helped offset apprehensions surrounding US trade policies. Preliminary data for February showed that Germany’s inflation rate remained steady at 2.8%, slightly above the anticipated 2.7%. Italy’s annual consumer price growth held at 1.7%, falling short of expectations, while France’s inflation rate dropped to a four-year low of 0.9% from the previous 1.8%. Concurrently, final estimates confirmed contractions in the fourth-quarter gross domestic product for both Germany (−0.2%) and France (−0.1%).

Japan: The core consumer price index in Tokyo rose by 2.2% year-on-year, slightly below forecasts, primarily due to the reintroduction of energy subsidies. Concurrently, factory activity contracted for the eighth consecutive month, with the Purchasing Managers’ Index (PMI) inching up to 49.0 from January’s 48.7, remaining below the growth threshold of 50.0. Despite these challenges, the Bank of Japan (BOJ) maintained its stance on monetary policy, indicating readiness to adjust interest rates further if inflation trends persist.

China: The government reaffirmed its commitment to achieving a 5% GDP growth target for the year, despite escalating trade tensions with the United States, which imposed additional tariffs on Chinese imports. In response, China announced retaliatory measures, including tariffs on US goods and restrictions on certain exports. Domestically, manufacturing activity showed signs of recovery, with the Purchasing Managers’ Index (PMI) expanding at its fastest pace in three months, driven by increased orders and purchasing volumes. However, external pressures from the ongoing trade disputes pose significant risks to China’s export performance and overall economic stability.

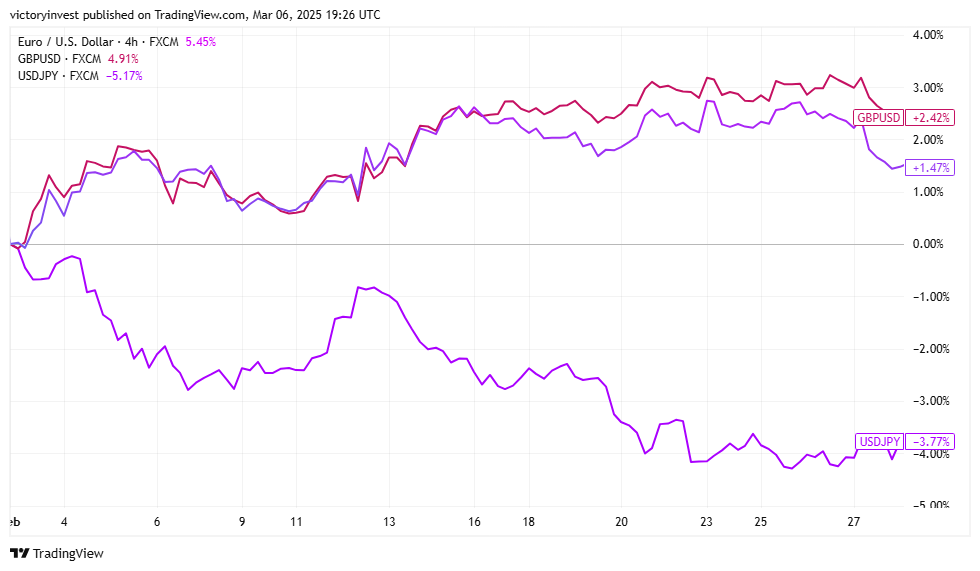

EURUSD GBPUSD USDJPY Performance – February 2025

The Portfolio Management Team